France's 2026 Real Estate Forecast, 5 Months In

Tariffs, Middle East conflict and a late budget reshaped the picture.

Last January, the property advisers CBRE published their outlook for French real estate in 2026. Five months on, it’s a useful moment to ask how well it has held up.

France finally passed a national budget in February, after months of deadlock. Municipal elections took place in March. And from outside France, three external shocks landed: the fallout from US tariffs, conflict in the Middle East, and the higher energy prices it brought.

Here’s where the forecast stands at the end of May.

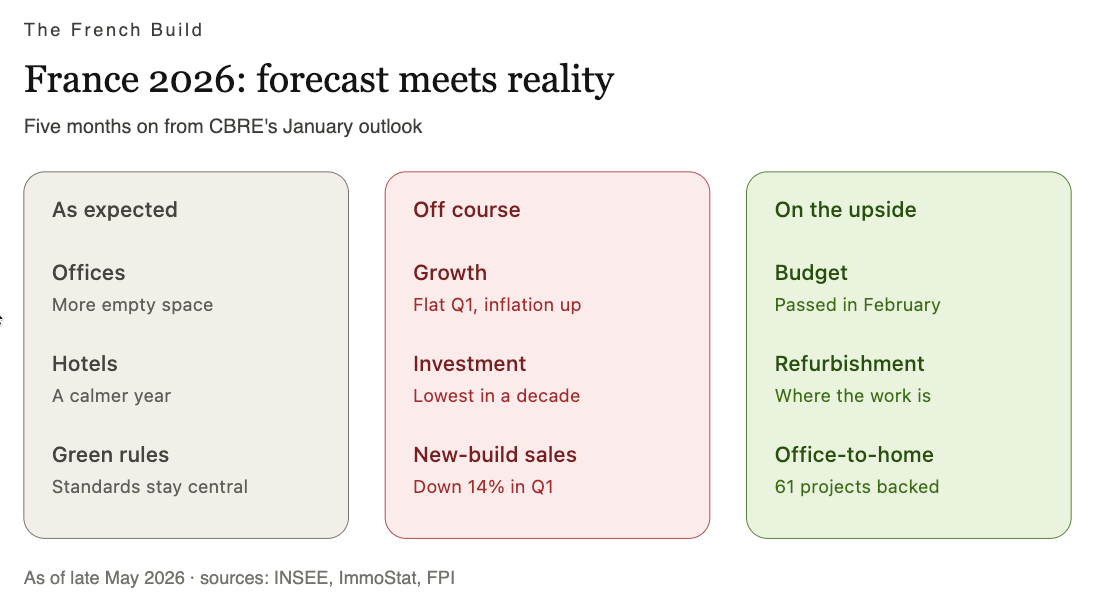

Three things that went more or less as expected

Offices. CBRE expected empty office space to keep building up, and it has. Available space in the Paris region is up about 9% on a year ago, with roughly one square metre in ten sitting vacant. Demand for new offices remains thin.

Hotels. After a record 2025, CBRE expected a calmer year, and that’s what we’ve seen. Occupancy softened in the first quarter, though room rates held up and Paris stayed resilient.

Green building regulations. CBRE expected environmental standards to stay central even as Brussels eased some company reporting duties. They have. France’s tighter carbon limits for new buildings took effect on schedule; a building’s energy performance still shapes what tenants and investors will pay for it.

Three things that went in the wrong direction

Economic growth. CBRE forecast about 1% for the year, but the economy was flat in the first quarter. That owed more to a fall in construction and the local election cycle than to events abroad. However, the rise of inflation to 2.2% in April was linked to oil price increases, and to shipping disruption in the Strait of Hormuz. That has push up the cost of energy-intensive building materials, such as glass, steel and ceramics.

Investment dried up. Money going into French commercial property fell to its lowest first quarter in ten years, down roughly half on a year earlier. Logistics warehouses were hit hardest. CBRE had expected a slow recovery, not a fresh slump.

New-build sales keep falling. The hoped-for new-build housing rebound hasn’t happened. Sales of new homes fell over 14% in the first quarter, and bulk sales to social landlords, a figure CBRE watched closely, dropped by a third.

Three things to be positive about

The budget. The single biggest uncertainty CBRE flagged, an unresolved national budget, is now behind us. It passed in February. The process was messy, but the question mark has gone.

Refurbishment continues. Across almost every sector, new building is quiet while renovation and reuse are picking up. For anyone in design, engineering or building products, that’s where the steady demand now sits.

Office-to-home conversion. With so much empty office space, converting it into housing is finally getting real support: the state is backing 61 conversion projects in the Paris region. Delivery is still slow, but the legal groundwork is now in place.

In short

CBRE read the fundamental trends well: weak demand, oversupplied offices, a flight to quality, and a shift towards reuse over new-build.

What no January forecast could fully price in were the external shocks: the conflict in the Middle East drove inflation up and froze investment. However, the flat first quarter owed more to home-grown factors: a fall in construction, the election cycle and a mild winter.

The direction CBRE described still holds, but the timing has slipped. We may have to wait until 2027 for growth and investment to turn back up.